The headline picture

Research on entrepreneurial finance focuses overwhelmingly on how much capital founders raise, treating a dollar as a dollar. We argue that, in crowdfunding, the social composition of capital—who the money comes from—carries information and obligations that shape a venture's trajectory independently of the amount raised.

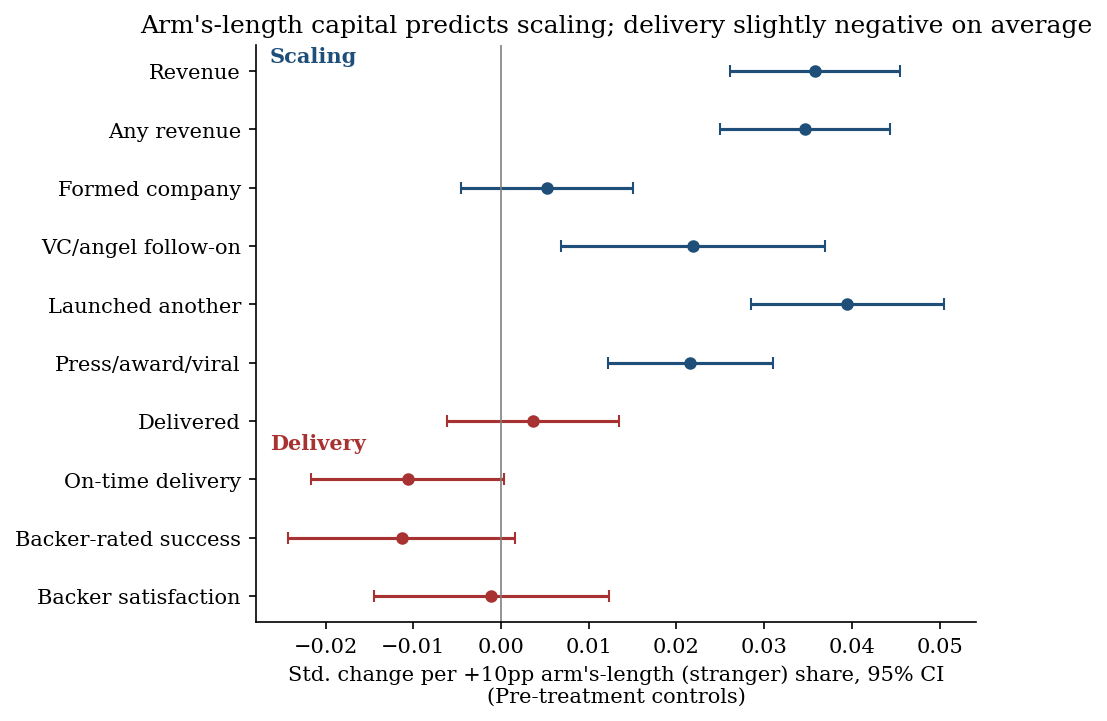

Using a survey of 8,243 funded Kickstarter creators who each reported the share of their funding that came from family and friends, from existing communities, and from complete strangers, merged with archival campaign data, we document an "embeddedness gradient."

Holding the amount pledged, the goal, the number of backers, category, and timing constant, a larger share of arm's-length (stranger) capital predicts about 16% higher post-campaign revenue per +10 percentage points (and roughly 4.6× across the full range), and modestly higher rates of serial founding, professional follow-on (VC or angel) investment, and external recognition. Decomposing embeddedness, family-and-friends capital is the growth laggard while community and stranger capital both outperform it. Direct Wald tests show the community-vs-stranger differences are only marginally significant (p = 0.07–0.13), so the “community sweet spot” is best read as a directional pattern: community sits closer to stranger capital on growth and closer to no-effect on delivery, but the cross-category differences are not always statistically distinguishable.

These are conditional associations from a retrospective survey of funded projects, not causal effects. Unobserved founder ambition, product-market fit, and pre-existing audience could explain part of the pattern.

Holding the amount raised constant, +10pp of stranger funding is associated with a 0.066 log-point increase in post-campaign revenue (p < 0.001) and higher rates of company formation, VC/angel follow-on, serial founding, and press — a textbook coefficient-stability pattern (b drops from 0.170 to 0.066 once size is controlled, then stays put).

Family-and-friends capital is the growth laggard; community and stranger capital both outperform it. Community sits directionally above stranger capital on delivery and below it on VC/angel follow-on, but Wald tests of community = stranger return only marginal p-values (0.07–0.13). The gradient is consistent with Uzzi's paradox; the four-cell typology is suggestive rather than statistically sharp.

In larger campaigns, the company-formation premium from arm's-length capital grows significantly (interaction b = +0.019, p = 0.016). The mirror-image on-time delivery cost moves in the predicted direction but does not reach conventional significance (b = −0.015, p = 0.12; CEM at p = 0.06). The growth half of the trade-off is confirmed; the delivery half is suggestive.

Crowdfunding can democratize access to money, but our results suggest it does not thereby democratize access to growth: projects financed mainly by friends and family — the founders for whom crowdfunding is meant to compensate for missing market access — are the least likely to scale.

We measure, for each funded creator, the dollar-weighted shares of funding from (i) family and friends, (ii) communities the creator belongs to, and (iii) complete strangers, normalized to sum to one. The three components sum to 100±5 for 73% of respondents, and dollar-share and backer-count versions of each source correlate at r ≈ 0.95, supporting the measure's internal and convergent validity.

All models control for the (log) amount pledged, (log) goal, (log) backers, a video indicator, a U.S. indicator, (log) updates and comments, and category and launch-year fixed effects, with standard errors clustered by creator. Identification is supported by a specification ladder showing coefficient stability, coarsened exact matching, entropy balancing, Oster δ coefficient-stability bounds (1.5 for revenue, 3.7 for serial founding), and alternative estimators (Poisson/PPML, ordered logit, logit average marginal effects) that all yield substantively identical results. Estimates are framed as conditional associations.